Examine notebook used to visualize results¶

First we will load the endpoint name, training time, prediction length and seom of the data

%store -r

print('endpoint name ', endpoint_name)

print('end training', end_training)

print('prediction_length', prediction_length)

endpoint name DeepAR-forecast-taxidata-2019-11-30-16-26-45-053

end training 2019-05-06 00:00:00

prediction_length 14

Sample data being used:¶

print('data sample')

ABB.head(5)

data sample

| green | yellow | full_fhv | |

|---|---|---|---|

| ts_resampled | |||

| 2018-01-01 | 23292 | 237118 | 702058.0 |

| 2018-01-02 | 23222 | 238152 | 547447.0 |

| 2018-01-03 | 26417 | 266992 | 583735.0 |

| 2018-01-04 | 6519 | 122222 | 354626.0 |

| 2018-01-05 | 27453 | 265212 | 699966.0 |

This next cell creates the predictor using the endpoint_name. Ideally we’d have the DeepARPredictor in a seperate .py rather than repeated in the two notebooks.

import sagemaker

from sagemaker import get_execution_role

from sagemaker.tuner import HyperparameterTuner

import numpy as np

import json

import pandas as pd

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

class DeepARPredictor(sagemaker.predictor.RealTimePredictor):

def __init__(self, *args, **kwargs):

super().__init__(*args, content_type=sagemaker.content_types.CONTENT_TYPE_JSON, **kwargs)

def predict(self, ts, cat=None, dynamic_feat=None,

num_samples=100, return_samples=False, quantiles=["0.1", "0.5", "0.9"]):

"""Requests the prediction of for the time series listed in `ts`, each with the (optional)

corresponding category listed in `cat`.

ts -- `pandas.Series` object, the time series to predict

cat -- integer, the group associated to the time series (default: None)

num_samples -- integer, number of samples to compute at prediction time (default: 100)

return_samples -- boolean indicating whether to include samples in the response (default: False)

quantiles -- list of strings specifying the quantiles to compute (default: ["0.1", "0.5", "0.9"])

Return value: list of `pandas.DataFrame` objects, each containing the predictions

"""

prediction_time = ts.index[-1] + 1

quantiles = [str(q) for q in quantiles]

req = self.__encode_request(ts, cat, dynamic_feat, num_samples, return_samples, quantiles)

res = super(DeepARPredictor, self).predict(req)

return self.__decode_response(res, ts.index.freq, prediction_time, return_samples)

def __encode_request(self, ts, cat, dynamic_feat, num_samples, return_samples, quantiles):

instance = series_to_dict(ts, cat if cat is not None else None, dynamic_feat if dynamic_feat else None)

configuration = {

"num_samples": num_samples,

"output_types": ["quantiles", "samples"] if return_samples else ["quantiles"],

"quantiles": quantiles

}

http_request_data = {

"instances": [instance],

"configuration": configuration

}

return json.dumps(http_request_data).encode('utf-8')

def __decode_response(self, response, freq, prediction_time, return_samples):

# we only sent one time series so we only receive one in return

# however, if possible one will pass multiple time series as predictions will then be faster

predictions = json.loads(response.decode('utf-8'))['predictions'][0]

prediction_length = len(next(iter(predictions['quantiles'].values())))

prediction_index = pd.DatetimeIndex(start=prediction_time, freq=freq, periods=prediction_length)

if return_samples:

dict_of_samples = {'sample_' + str(i): s for i, s in enumerate(predictions['samples'])}

else:

dict_of_samples = {}

return pd.DataFrame(data={**predictions['quantiles'], **dict_of_samples}, index=prediction_index)

def set_frequency(self, freq):

self.freq = freq

def encode_target(ts):

return [x if np.isfinite(x) else "NaN" for x in ts]

def series_to_dict(ts, cat=None, dynamic_feat=None):

"""Given a pandas.Series object, returns a dictionary encoding the time series.

ts -- a pands.Series object with the target time series

cat -- an integer indicating the time series category

Return value: a dictionary

"""

obj = {"start": str(ts.index[0]), "target": encode_target(ts)}

if cat is not None:

obj["cat"] = cat

if dynamic_feat is not None:

obj["dynamic_feat"] = dynamic_feat

return obj

predictor = DeepARPredictor(endpoint_name)

import matplotlib

import matplotlib.pyplot as plt

def plot(

predictor,

target_ts,

cat=None,

dynamic_feat=None,

forecast_date=end_training,

show_samples=False,

plot_history=7 * 12,

confidence=80,

num_samples=100,

draw_color='blue'

):

print("Calling endpoint to generate {} predictions starting from {} ...".format(target_ts.name, str(forecast_date)))

assert(confidence > 50 and confidence < 100)

low_quantile = 0.5 - confidence * 0.005

up_quantile = confidence * 0.005 + 0.5

# we first construct the argument to call our model

args = {

"ts": target_ts[:forecast_date],

"return_samples": show_samples,

"quantiles": [low_quantile, 0.5, up_quantile],

"num_samples": num_samples

}

if dynamic_feat is not None:

args["dynamic_feat"] = dynamic_feat

fig = plt.figure(figsize=(20, 6))

ax = plt.subplot(2, 1, 1)

else:

fig = plt.figure(figsize=(20, 3))

ax = plt.subplot(1,1,1)

if cat is not None:

args["cat"] = cat

ax.text(0.9, 0.9, 'cat = {}'.format(cat), transform=ax.transAxes)

# call the end point to get the prediction

prediction = predictor.predict(**args)

# plot the samples

mccolor = draw_color

if show_samples:

for key in prediction.keys():

if "sample" in key:

prediction[key].asfreq('D').plot(color='lightskyblue', alpha=0.2, label='_nolegend_')

# the date didn't have a frequency in it, so setting it here.

new_date = pd.Timestamp(forecast_date, freq='d')

target_section = target_ts[new_date-plot_history:new_date+prediction_length]

target_section.asfreq('D').plot(color="black", label='target')

plt.title(target_ts.name.upper(), color='darkred')

# plot the confidence interval and the median predicted

ax.fill_between(

prediction[str(low_quantile)].index,

prediction[str(low_quantile)].values,

prediction[str(up_quantile)].values,

color=mccolor, alpha=0.3, label='{}% confidence interval'.format(confidence)

)

prediction["0.5"].plot(color=mccolor, label='P50')

ax.legend(loc=2)

# fix the scale as the samples may change it

ax.set_ylim(target_section.min() * 0.5, target_section.max() * 1.5)

if dynamic_feat is not None:

for i, f in enumerate(dynamic_feat, start=1):

ax = plt.subplot(len(dynamic_feat) * 2, 1, len(dynamic_feat) + i, sharex=ax)

feat_ts = pd.Series(

index=pd.DatetimeIndex(start=target_ts.index[0], freq=target_ts.index.freq, periods=len(f)),

data=f

)

feat_ts[forecast_date-plot_history:forecast_date+prediction_length].plot(ax=ax, color='g')

Let’s interact w/ the samples and forecast values now.¶

from __future__ import print_function

from ipywidgets import interact, interactive, fixed, interact_manual

import ipywidgets as widgets

from ipywidgets import IntSlider, FloatSlider, Checkbox, RadioButtons

import datetime

style = {'description_width': 'initial'}

@interact_manual(

series_type=RadioButtons(options=['full_fhv', 'yellow', 'green'], value='yellow', description='Type'),

forecast_day=IntSlider(min=0, max=100, value=21, style=style),

confidence=IntSlider(min=60, max=95, value=80, step=5, style=style),

history_weeks_plot=IntSlider(min=1, max=20, value=4, style=style),

num_samples=IntSlider(min=100, max=1000, value=100, step=500, style=style),

show_samples=Checkbox(value=True),

continuous_update=False

)

def plot_interact(series_type, forecast_day, confidence, history_weeks_plot, show_samples, num_samples):

plot(

predictor,

target_ts=ABB[series_type].asfreq(freq='d', fill_value=0),

forecast_date=end_training + datetime.timedelta(days=forecast_day),

show_samples=show_samples,

plot_history=history_weeks_plot * prediction_length,

confidence=confidence,

num_samples=num_samples

)

interactive(children=(RadioButtons(description='Type', index=1, options=('full_fhv', 'yellow', 'green'), value…

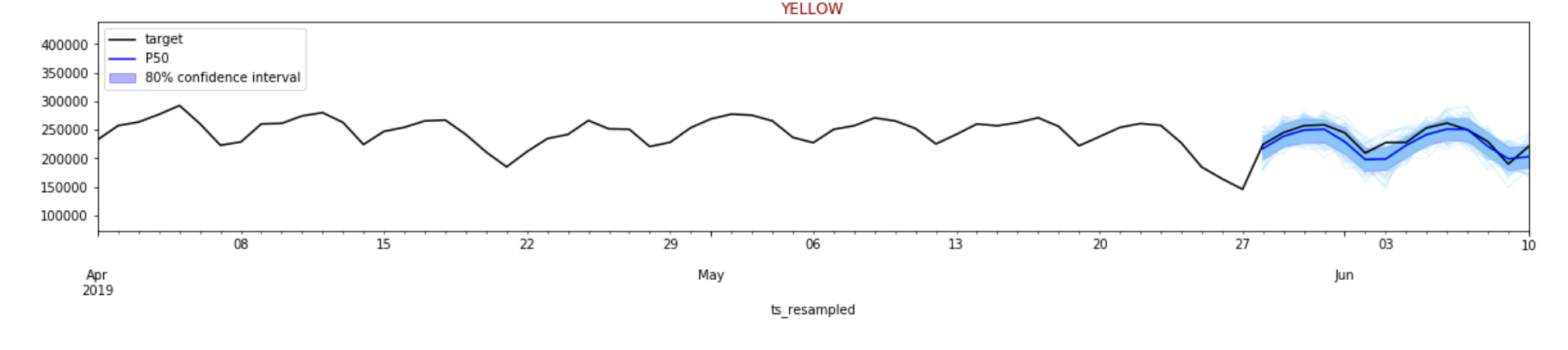

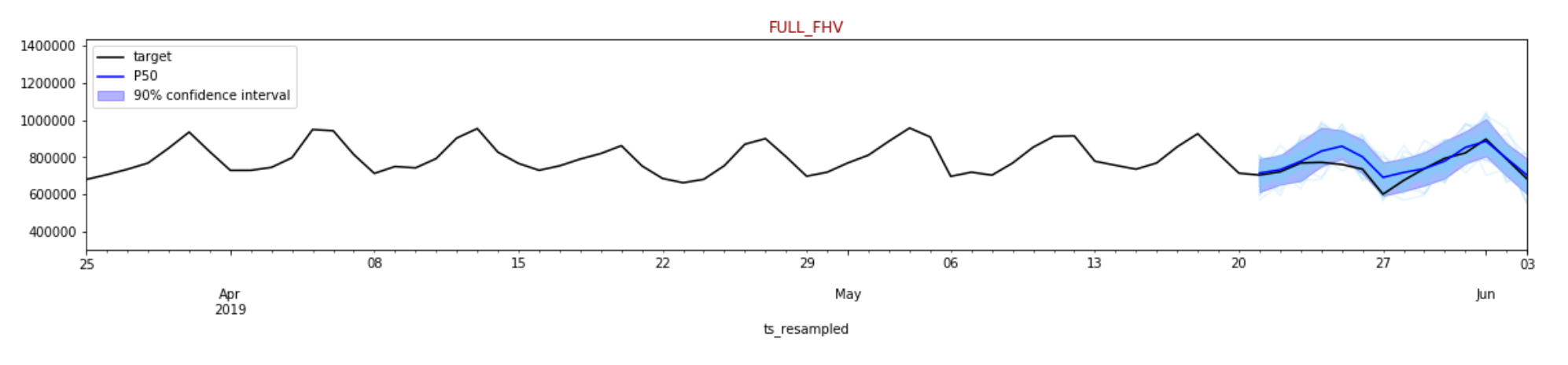

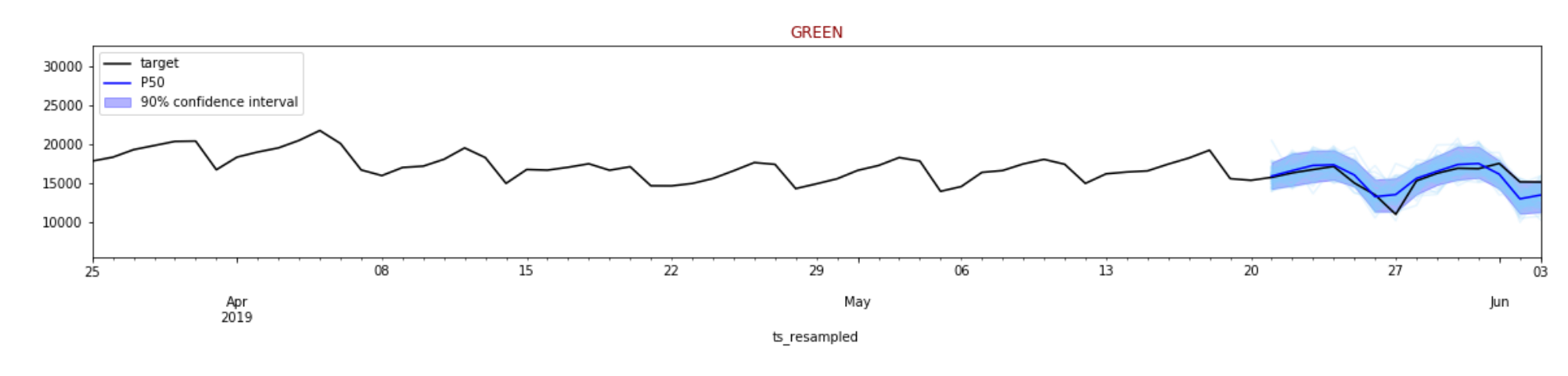

Testing and Understanding the results¶

You can test the results and see different results. Here are some examples below: